Outlook 2026: industrial sector will outperform across Europe

Industrial and logistics are set to outperform all other asset classes, with industrials delivering the strongest segment performance within the sector, delegates heard at Real Asset Media’s European Outlook 2026, which took place in Copenhagen this week.

“The case for investing in industrial and logistics real estate remains compelling across asset types and investment risk strategies”, said Troels Andersen, Head of Funds Europe & Fund Manager, Aberdeen Investments, in his keynote presentation. “There is a structural rather than cyclical change underway that supports the sector”.

The conviction call is driven by economic transformation trends, changes in Europe’s industrial landscape and supportive policy decisions at national and EU level.

“European countries have realised they need to be more self-reliant, there is a strong political push to produce more in Europe and this is leading to supply chain reconfiguration”, he said. “The goals are greater economic sovereignty and resilience, and this shift is having a huge impact on the I&L sector.”

Industrial production is also set to receive a boost from EU policy decisions, as structural shifts are underway in EU policy, fiscal easing and defence spending to supplement cyclical recovery.

Just to give an example, currently 95% of solar panels installed in the EU are produced in China, but by law at least 40% will have to be produced in the EU by 2030.

“This policy driver will have a strong impact on the need for modern production facilities”, Andersen said. “Another big driver is defence spending, which is set to increase and will lead to demand for 1,500 brand new assets across Europe.”

The nearshoring trend, now more often called ‘friendshoring’, continues, driven by cost, resilience & ESG and the wish to be close to customers. This is having a positive, if uneven, impact on EU countries, as there will be a concentration of demand in some locations.

“CEE and mature Western European markets like Germany, France and Benelux are set to benefit, while higher-cost and more remote markets, such as the Nordics, will not benefit as much”, said Andersen.

The supply and demand fundamentals are also very supportive, said Andersen: “ “Across Europe there’s a reluctance to allow new developments in greenfield areas, so supply is limited and rental growth likely.”

There is also likely to be more investment in old stock: until recently it was not worth deploying money in outdated assets, but the increasing demand for modern, ESG-compliant assets is leading to more upgrades and renovations.

“There’s a lot of capital out there that had been sitting on the sidelines for the last couple of years”, said Andersen. “Now is the right time to invest in I&L.”

Benefits for investors include the wide range of property types, the value creation opportunities in ESG transformation, strong performance characteristics, shorter income to capture reversion potential and longer-term inflation linked leases.

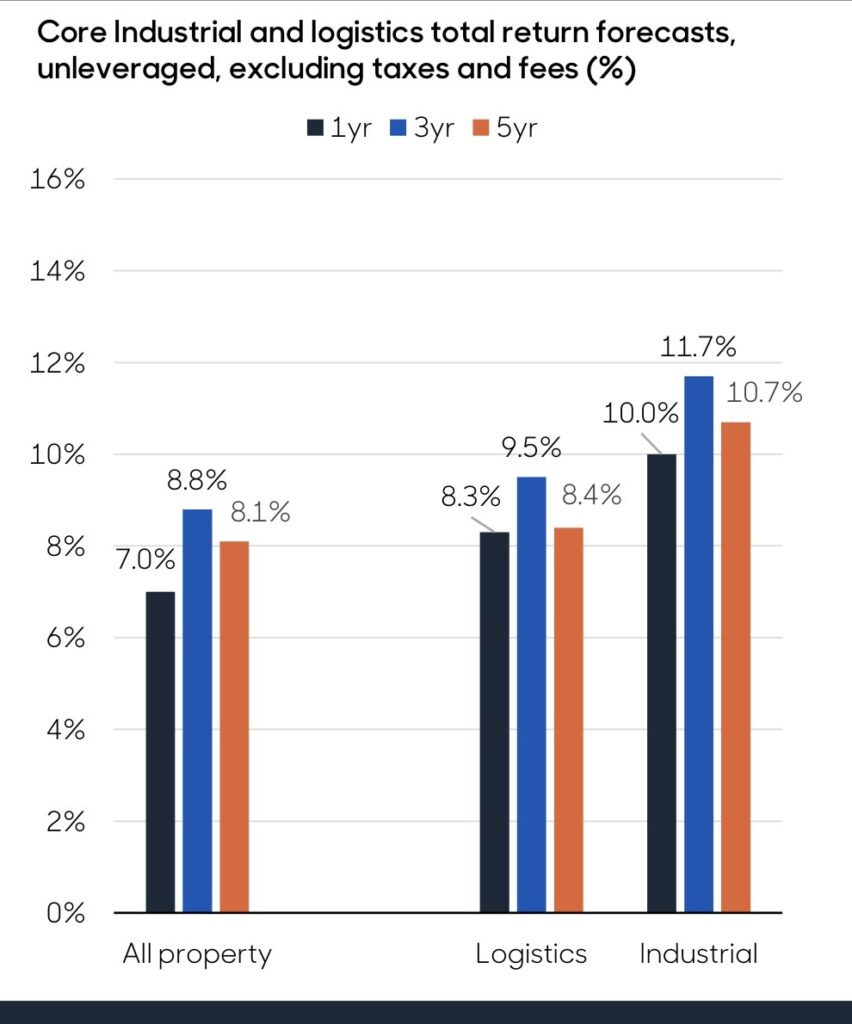

“The I&L sector has delivered strong returns in the last 20 years and we expect a similar performance over the next five years”, said Andersen. “We are looking at 8-10% total returns, which are very attractive in a low-interest rate environment.”