‘The customer is king, now more than ever’

PwC’s annual consumer insights report highlights how the retail sector and shopping habits have undergone seismic changes since the onset of the pandemic. Nicol Dynes reports.

The customer is king: that age-old business mantra has been given new relevance and meaning this year, as the rapid changes brought about by the pandemic have put the consumer at the centre of everything. To remain relevant and successful, retailers will have to understand and provide what customers now want.

This is what emerges from PwC’s 11th annual Global Consumer Insights Survey, The consumer transformed, published earlier this month. The report focuses on urban dwellers because the concentration of billions of people in cities has “created a new era of global consumption”, says PwC.

Not only are cities “vibrant centres of education and innovation, seedbeds and green houses for new ideas”, they are also where economic activity happens. As the World Bank notes, 80% of global GDP is generated in cities, so it is crucial for businesses to understand the behaviour of city consumers.

Interestingly, PwC polled city dwellers on their shopping behaviour both before and after the pandemic, to pinpoint and track any changes in attitude and habits with a particular focus on Europe, China and the Middle East.

Consumers spending less

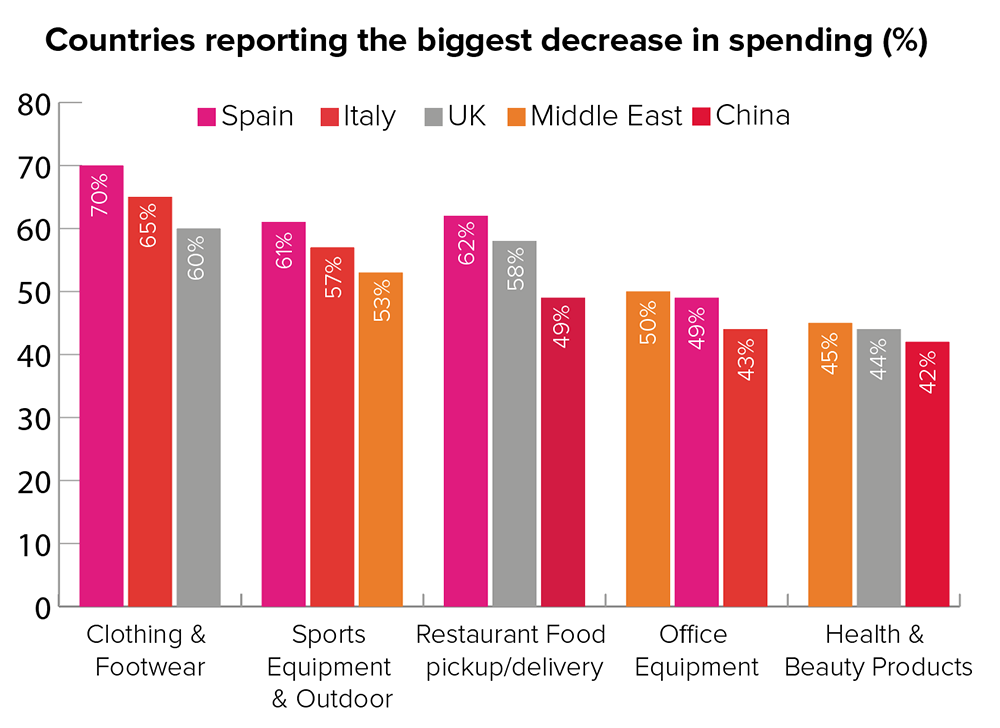

One immediate change that Covid-19 and its economic impact has brought about is a tightening of the purse strings. Consumers are spending less in all non-food categories: 51% less on clothing and footwear, 46% less on sports equipment and outdoor activities, 41% less on restaurant food, including take-out and delivery, 36% less on office equipment and 35% less on beauty products.

Since the outbreak, people have been spending the most on groceries, in-place entertainment and home projects. They are also making fewer trips to supermarkets or grocery stores, favouring bigger but less frequent shopping trips. They are spending less on non-food items and buying online.

The pandemic has drastically changed people’s outlook: before the outbreak consumer confidence was sky-high, with 46% of respondents expecting to spend more over the next 12 months. After the outbreak, 40% of global consumers reported a fall in income due to job loss or redundancy and 41% said their household bills had increased.

The percentage of people who said they would spend more fell by 10%, while the number of people who plan to spend less almost doubled to 36%. Spain, the UK and Italy are the countries with the biggest numbers of consumers facing difficulties, while the Middle East, China and France have the most resilient shoppers who plan to spend more.

There are signs that consumer confidence is returning in places where the pandemic is being handled most efficiently, or the perception is that the worst is over. “Our own Covid-19 consumer study shows that the spending outlook is more positive in countries where isolation measures are being lifted, such as China and the Middle East,” states the report.

How companies should react

In most countries, though, businesses should expect market volatility and price sensitivity, as customers’ buying habits will be changeable and price and value will become paramount considerations.

To address these issues, companies should understand what shoppers really value to determine the minimum viable basket, the ‘anchor’ products or services that must be available at all times and prioritised through the supply chain. They should then focus assortments and promotions on this core basket, as well as ensure that the supply chain has been recalibrated to maintain delivery of products for this core basket.

Businesses should also make an effort to understand how customers’ priorities are changing to put more weight on price and value, and use this opportunity to re-evaluate their relationship with their customers, also considering new pricing strategies and loyalty programmes in the digital ecosystem to drive and maintain customer engagement.

Safety and accessibility are also crucial, as companies must ensure that consumers feel confident enough to return to a semblance of normal physical interaction with retailers, hotels and other consumer-facing businesses. Confidence in the brand, safety and cleanliness come out as the top considerations for customers.

The survey carried out after the pandemic hit shows that safety, security and healthcare have become as important as employment prospects in the list of reasons for choosing a city, while before the outbreak they lagged well behind the opportunity of finding a job.

Safety is also the reason people spend more time at home, which explains why the only increases in non-food spending are for home entertainment and media, DIY, home improvement and gardening.

The implication is that “companies with the technology and imagination to design great experiences in the home or close to home will have a huge advantage, at least in the short term”. As time goes by, however, there will be more opportunities for blended physical and virtual experiences.

The modern retail mixed-use retail environment is efficient, serving as a lifestyle destination encompassing green spaces, shops, restaurants, health and fitness, entertainment centres and fitness facilities, intertwined with transportation grids and higher-density urban residential and work communities.

This “localised, contained and safe ecosystem which can knit the community fabric closer together will be in high demand,” Ghaith Shocair, former CEO of Majid AL Futtaim Shopping Malls, a leading mall developer headquartered in Dubai, told PwC.

Mobile shopping accelerating

The other clear trend that emerges from the study is that when consumers do decide to spend their money, they do so on mobile platforms. The pandemic has not only accelerated the shift to online shopping, it has also encouraged experimentation, prompting consumers to explore different ways to access products and services.

Before the pandemic, mobile shopping was comparable to other forms of online shopping but since then it has grown in popularity. The 50% decline in in-store shopping is mirrored by the 45% increase in shopping online using a mobile phone, the 41% rise in online shopping via computer and the 33% increase in online shopping using a tablet.

Covid-19 has “greased the digital runway” and highlighted the ease, portability and immediacy of mobile shopping. A massive 93% of respondents say they are likely to maintain their current increased use of mobile phones for shopping after the health emergency is over, so it is not a passing fad.

More consumers have even turned to buying groceries online. “Buying fresh produce online, which was unfathomable to many a few months ago, has become the new normal,” says the report. Two-thirds of consumers are now doing their grocery shopping online and significantly, 86% of respondents said they will continue to do so after social distancing measures have been removed.

However, it would be premature to write off physical stores, an experience that consumers continue to value, especially in Germany, France and the Netherlands. The report emphasises that “the overarching trend will be towards an omnichannel experience, with consumer-facing companies needing to seamlessly integrate their offline and online experiences”.

A clear convergence of themes

The billion dollar question is whether the changes of the last few months, from remote working to online shopping, will become permanent or whether consumers will return to old habits once the health crisis is over.

Understanding which changes are transient and which permanent puts companies in a position to navigate disruption. Some trends are likely to become fixtures, like more working from home, an increased use of video chat apps, an openness to sharing data and an increased awareness of environmental issues, reducing waste and avoiding the use of plastic whenever possible. The seismic shift towards self-care, more attention to fitness and mental and physical health, will also not be reversed.

“The phenomenon of a care-centric customer base and business culture could truly be the silver lining in the Covid-19 pandemic,” says PwC. Businesses should develop new, sustainable products and services, establish greater inclusivity and transparency across supply chains, increase R&D investment in the future of food and nutrition and train staff to provide a consistent service in line with the brand. They should also work together with NGOs, the media, trade associations and academia to re-examine the values they espouse and the actions they take.

The level of scrutiny has increased: consumers hold companies accountable for their actions and can be harsh judges, but they also will also reward with loyalty companies that meet or exceed their expectations.

PwC research points to an increased desire for transparency, sustainability, cleanliness, community living and social consciousness. The road ahead is clear, says the report: “In our 11 years of surveying consumers around the globe, we have never documented such a clear convergence of themes.”

All consumer-facing companies must establish trust with the consumer. “Our insight suggests that the pace of change and industry disruption underway will drive the emergence and establishment of a new cohort of winners and laggards over the next decade, with the consumer at the centre as never before.”

‘The pandemic has not only accelerated the shift to online shopping, it has also encouraged experimentation, prompting consumers to explore different ways to access products and services.’

The pandemic and subsequent lockdowns have brought a move to more local community-focused retail