Listed real estate’s guide for sustainability reporting

What began as a niche guidance tool has matured into the only pan-European ESG disclosure standard built for listed real estate. Lourdes Calderón Ruiz reports.

When EPRA launched its Sustainability Best Practices Recommendations (sBPR) in 2011, the listed real estate (LRE) sector faced a fragmented and inconsistent ESG reporting landscape.

There was no standardised approach tailored to the dual identity of LRE companies as both corporate entities and asset owners. The EPRA sBPR emerged to fill that void, grounded in the international standards organisation the Global Reporting Initiative (GRI), and aimed at promoting transparency, consistency and comparability in sustainability disclosures among LRE companies.

They were developed by a committee of experts, including leaders from listed real estate companies and institutional investors, ensuring the framework reflected both industry realities and investor expectations.

Over the years, this voluntary framework gained significant traction and evolved into a widely adopted reference across Europe. By 2024, more than 70% of the world’s top 100 companies were reporting under GRI standards, reaffirming the relevance of EPRA’s alignment strategy. What began as a niche guidance tool has matured into the only pan-European ESG disclosure standard built for LRE.

As the framework became more deeply embedded in the sector, the regulatory landscape began to shift. In 2023, the European Commission adopted the first set of European Sustainability Reporting Standards (ESRS) under the Corporate Sustainability Reporting Directive (CSRD), with the first wave of large and listed companies required to begin reporting for financial years starting on or after 1 January 2024.

These new standards, while comprehensive, were sector-agnostic and not tailored to the operational complexities of real estate. Recognising the need to support members through this regulatory shift, EPRA responded swiftly with a comprehensive mapping exercise in 2024.

Preparing for CSRD compliance

This analysis compared the EPRA sBPR with the sector-agnostic ESRS to identify areas of alignment and divergence. The aim was to provide real estate companies with clarity on how to reconcile voluntary industry practices with mandatory reporting requirements, and to help them start preparing more confidently for CSRD compliance.

As a result of this effort, EPRA published the fourth edition of the EPRA sBPR guidelines in April 2024. The update included ‘Bridge Requirements’, from the EPRA sBPR to the ESRS, as well as flagged ESRS datapoints that are not mandatory under the sBPR, but are relevant to its indicators and necessary for CSRD-aligned reporting. This positioned the EPRA sBPR not only as a voluntary framework, but

as a practical and strategic complement to the ESRS.

Then, in early 2025, the European Commission proposed the Omnibus Simplification Package, which marked a turning point in the EU’s approach to sustainability reporting.

The package removed the mandate to develop sector-specific ESRS, confirming that the sector agnostic/generalist standards would remain the only reference under CSRD going forward. While the policy change aimed to simplify compliance and reduce administrative burden, it created a critical gap for sectors like LRE that require tailored guidance.

Growing relevance of EPRA sBPR

For companies in this space, characterised by complex assets, regulatory oversight, and operational diversity, the absence of sector-specific standards makes the EPRA sBPR more relevant than ever. It now stands as the only structured, real estate-specific disclosure framework aligned with European regulatory expectations.

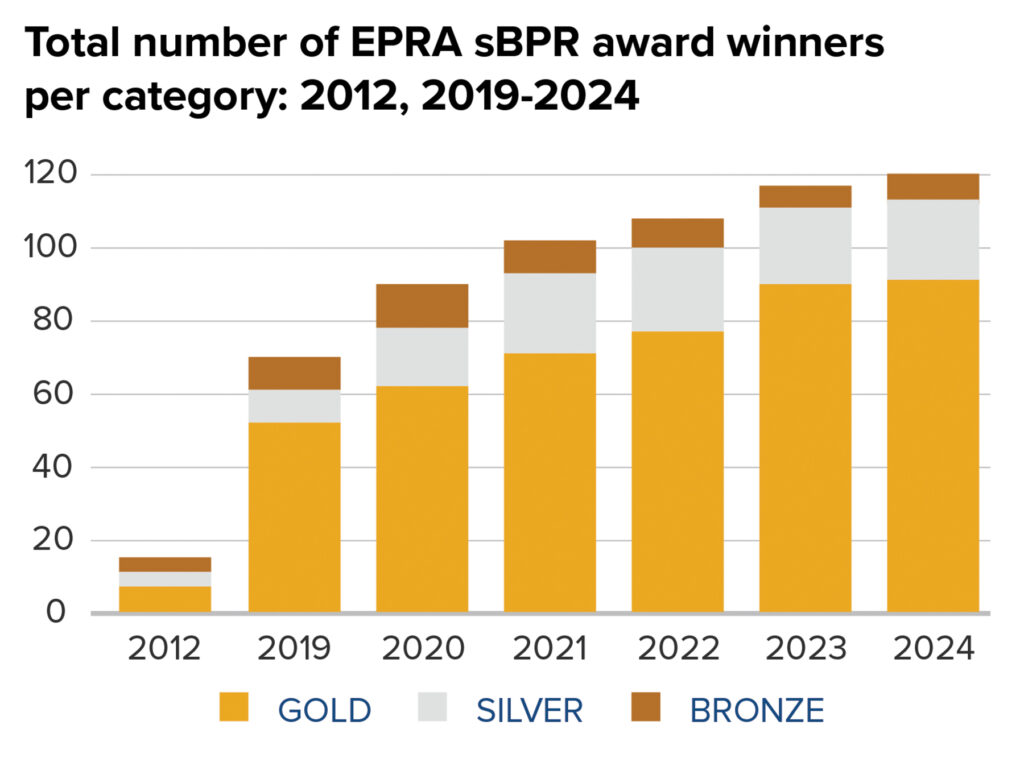

This growing relevance is clearly reflected in the 2024 EPRA sBPR Annual Survey report, Adapting and Adopting, which showcases the sector’s increasing commitment to high-quality sustainability disclosures. A total of 71% of participating companies received an EPRA sBPR award for their disclosures, up from 68% the year before, with nearly half showing year-on-year improvements.

The number of companies reporting on all Environmental, Social, and Governance performance measures increased, with 54%, 44%, and 86% of members respectively meeting these full disclosure thresholds. And 20% of members reported on all performance measures across the three categories, a clear indication of the sector’s rising maturity.

New entrants and first-time award winners also underscored the growing appeal and credibility of the EPRA sBPR framework. These trends reinforce how the sBPR is being used not only to comply with expectations, but to drive continuous improvement and stakeholder confidence.

EPRA sBPR database

A key enabler of this progress is the EPRA sBPR database, which now contains more than a decade of high-quality, portfolio-level ESG disclosures. This database is freely accessible to all EPRA members through the EPRA website, with information available for download to support analysis.

Looking ahead, the 2025 EPRA sBPR assessment is already underway. The results will be presented at the EPRA Annual Conference in September, offering the sector a timely point of reference and practical insight at a moment when voluntary, sector-specific guidance has become not just valuable, but essential for navigating evolving reporting expectations.

The EPRA sBPR continues to stand not because it is required, but because it works. Built by and for the industry, it has evolved with the sector, proving its value through more than a decade of use. In a shifting regulatory landscape, it remains a trusted, real estate-specific tool, relevant, resilient, and essential.

Lourdes Calderón Ruiz is ESG manager at EPRA