Living sectors outperforming despite geopolitical turmoil and economic headwinds

There is one asset class that is still outperforming despite geopolitical instability and a low-growth environment, delegates heard at Real Asset Media’s ‘The living sector: transformation driving opportunity’ briefing, which was hosted by PwC in London.

“The living sector still has tailwinds”, said Gareth Lewis, Director, Real Estate M&A, PwC, in his keynote address. “The long-term drivers are demographics and affordability and there is a structural undersupply across Europe.”

The sector stands out in the current extended transition period, characterised by uncertainty and lack of capital commitments, when many historic tailwinds that had supported real estate, like low interest rates, are now reversed.

“On top of this real estate is in competition with infrastructure and private credit”, Lewis said. “We are going through a transition from real estate as a simple, capital-driven asset class to a much more complex, thematic, operational asset class. There is no such thing as passive holding anymore.”

Capital flows tell the story: the living sector is the largest by volume globally. According to CBRE’s latest figures, the living sector accounted for 26% of the €53 billion total investments in European real estate in Q1 this year, a record figure.

“The composition of capital coming into the sector also has changed and is now distinct from traditional institutional capital”, said Lewis. “Private equity, high net worth individuals and family offices are stepping in. They are looking for thematic investments and living sectors fit the bill.”

The first of several challenges is regulation, as cities from Paris to Barcelona to Berlin implement restrictive measures from rent controls to bans on new co-living schemes. Another is development viability, as high construction costs mean that many projects don’t even start. On the other hand, supply constraints support rental increases.

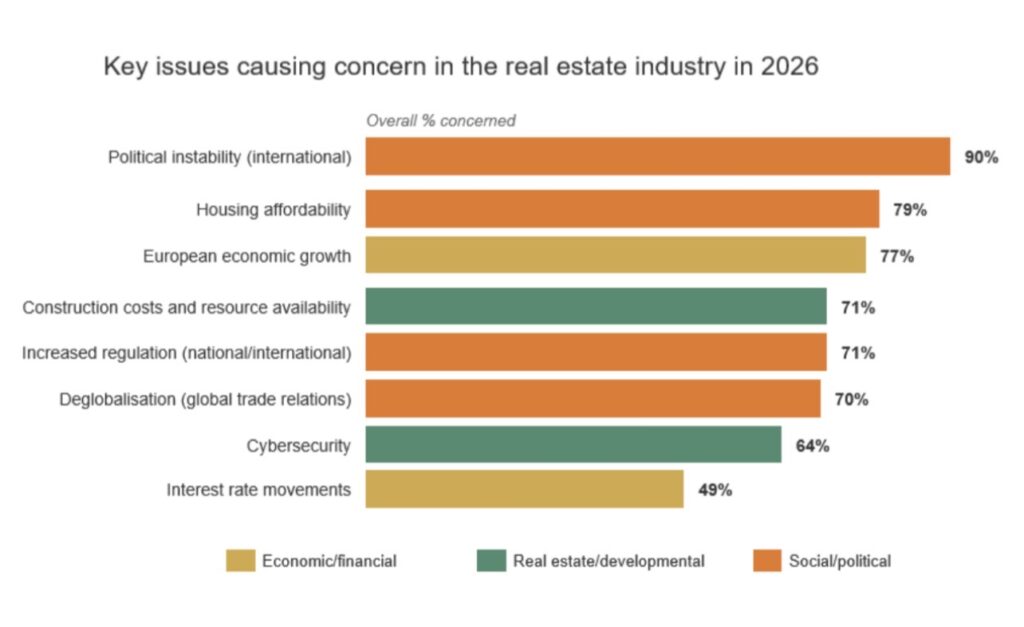

Housing affordability is the second concern among investors, just behind international political instability and ahead of (lack of) economic growth in Europe, according to PwC and ULI’s latest Emerging Trends in Real Estate survey.

Housing affordability has become a key issue, recognised by both individual governments and by the EU as a social and economic crisis and moving up the policy hierarchy. It is time to use all the levers at our disposal.

“This transition phase is a challenge and an opportunity for the real estate sector, that should fulfil its potential as an active enabler of economic growth”, said Lewis. “The industry is under pressure to up its game, and housing in particular should be the poster child of this transformation, at ground level and at policy and investor level.”