Savills: CEE logistics markets poised for long-term growth

Despite continuing uncertainty in Europe, I&L markets in CEE are poised for long-term growth, delegates heard at Trends 2025: Logistics investment opportunities in CEE, organised by Real Asset Media, Savills and MDC2, which took place at Savills’ headquarters in London on Wednesday.

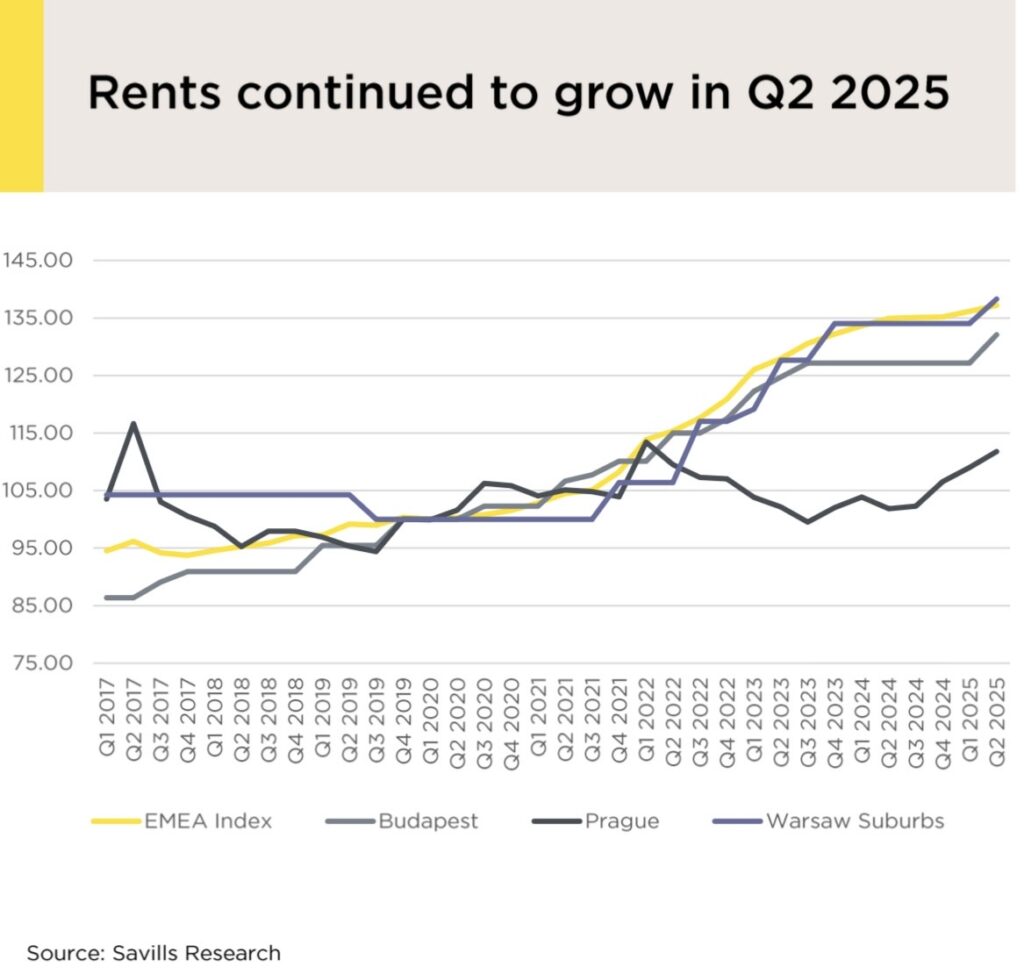

“In a context of general underperformance of the European market, both Poland and Budapest have seen a big increase in take-up this year”, said Andrew Blennerhassett, European Industrial & Logistics research analyst, Savills, in his keynote presentation. “But CEE markets are holding up very well and rents have continued to grow in Q2 2025.”

The bad news is that vacancy rates are up, but the good news is that the key driver of the increase has been spec developments. “There is a correction underway”, he said. “Spec developments in Poland have declined by over 50%, and in the Czech Republic and Budapest by double digits, and the fact that less stock in being developed supports rents.”

The CEE markets are underpinned by a strong economy and equally buoyant consumer sentiment. Poland, the stand-out country in the region, has consistently outperformed Europe on GDP growth in the last few years, with the sole exception of 2020, when the pandemic hit.

CEE countries also outperform Western Europe in consumer spending growth and they are expected to catch up on their online shopping habits. “E-commerce penetration rates are currently low, but this represents an opportunity to expand logistics markets”, said Blennerhassett. “There is plenty of growth runway in e-commerce in CEE markets.”

As the nearshoring trend continues, data show that Portugal, Poland and the Czech Republic are the stand-out countries in Europe. Looking ahead, another growth driver for the I&L sector is expected to be defence.

“CEE countries are already spending well above the 2% Nato target, especially Poland which is over 4%, a trend driven by proximity to Russia and heightened threat perception”, he said. Outside of Europe’s core defence markets like Germany, Italy, France and Spain, Sweden and Poland are set to see the biggest growth in defence spending.

“Pipeline development falling, nearshoring and the defence sector picking up and e-commerce taking off are the tailwinds that will propel the market forwards”, said Blennerhassett.

Savills’ recent Logistics Census showed that costs are identified as the biggest challenge. Occupier market conditions have overtaken the availability of debt as a key concern for investors. “CEE markets are a solution to this problem, as costs are much lower, especially the cost of energy and of the workforce, including skilled labour”, he said. “Labour in CEE is still excellent value and Poland is a stark contrast to Germany, where costs have gone up.”

Investors are waiting for uncertainty to recede and for occupier sentiment to improve, but they should make the most of a narrow window, said Blennerhassett: “They now have a unique opportunity to take advantage of tightening yields before the market turns.”