Bayes report: new lending for UK CRE up 11% in the last year

New lending for commercial real estate showed the first signs of recovery at the end of 2024, according to Bayes Business School’s latest bi-annual report, which was published yesterday.

“Last year was difficult for CRE lenders, who had to deal with continued market value uncertainties, existing non-performing loans, and a surge of loan repayments, while generating new business”, said Nicole Lux, Senior Research Fellow, Bayes Business School. “However, lenders intensified their efforts to increase lending volumes during the second half of the year with new loan pricing cuts, and increased loan-to-value ratios.”

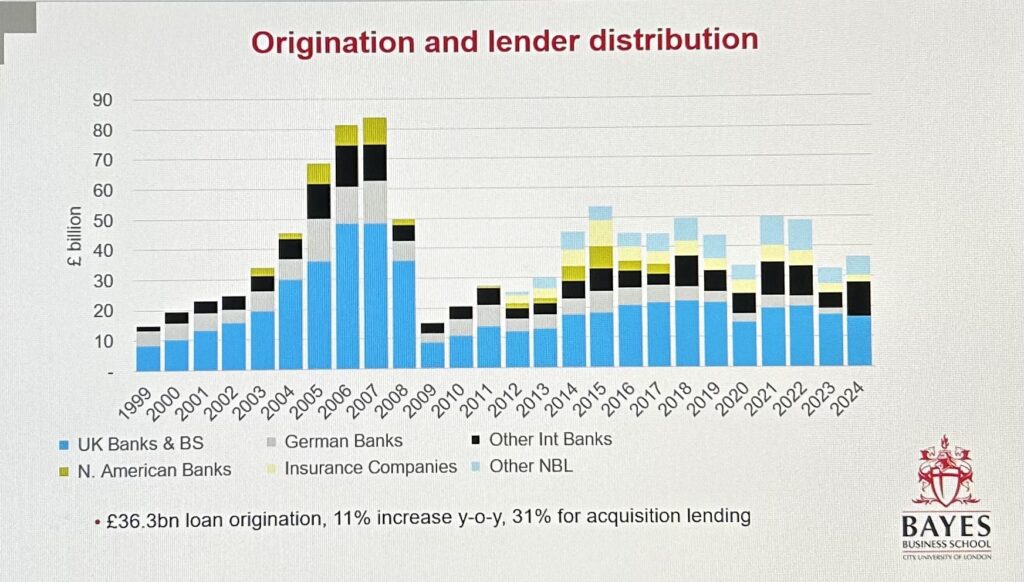

New CRE loan volumes increased by 11% year-on-year in the 12 months to 31 December 2024, reaching £36.3 billion. Most of the recovery was due to stronger lending activity during Q4 2024. The two base rate cuts during H2 2024 might have been one factor for the increased loan origination and recovery of the market during the second half of the year.

However, default loans on lenders’ books rose from 4.9% to 5.9% in just six months.

The year-end 2023 report highlighted that 34% of loans, valued at £57 billion, were due to mature in 2024. Data analysis for the report shows that 38% of new lending was funded through internal refinancing, while approximately 10% of loans that had already matured in 2024 were extended. That means some £32.6 billion of loans are expected to mature in 2025.

“For the best-in-class assets in the favoured sectors, there is plenty of liquidity and competition”, said Neil Odom-Haslett, President, the Association of Property Lenders. “LTVs have increased and spreads compressed and some lenders who were less active in 2022 and 2023 have returned. Given the challenging macroenvironment It’s not surprising that there was an increase in non-performing loans but the report does show that lenders are still disciplined in their underwriting.”

UK banks accounted for 46% of new loans during 2024, with international banks – particularly those with branches in London – providing 31%. The international banks with London branches were particularly active during the 2nd half of 2024. Debt funds only contributed 17% of new lending.

International banks boosted their activity in the UK, providing 36% of all speculative development finance. However, their targeted projects are mostly concentrated in London office schemes.

UK banks supplied 56% of all residential development finance and 28% of all other commercial development finance in the market. They also remain the strongest lender in all regional markets. The regional markets are well covered by UK retail banks, which lend 65% in the regions.

“The 2024 Bayes CRE Lending Report highlights how lender competition has driven significant margin compression, particularly for prime assets, creating opportunities – but also complexities – for borrowers navigating refinancing”, said John Hardie, Senior Director Debt & Structured Finance, CBRE. “With 38% of lending activity linked to refinancing and a wide divergence in terms across lender types, a deep understanding of market dynamics, lender appetite and evolving credit conditions is essential.”