Lack of supply in Paris market drives investors away from core

High demand and lack of supply in the Paris office market are is leading institutional investors to go up the risk curve, experts agreed at Real Asset Media’s France Investment Briefing, which took place recently on the REALX.Global platform.

“We are seeing a change in investment strategies, away from core and up the risk curve,” said Simon Wallace, head of research, alternatives, Europe, DWS. “Taking on redevelopment risk doesn’t seem so risky in Paris, as we still see high occupier demand and rental growth, especially for quality space that is ESG-compliant.”

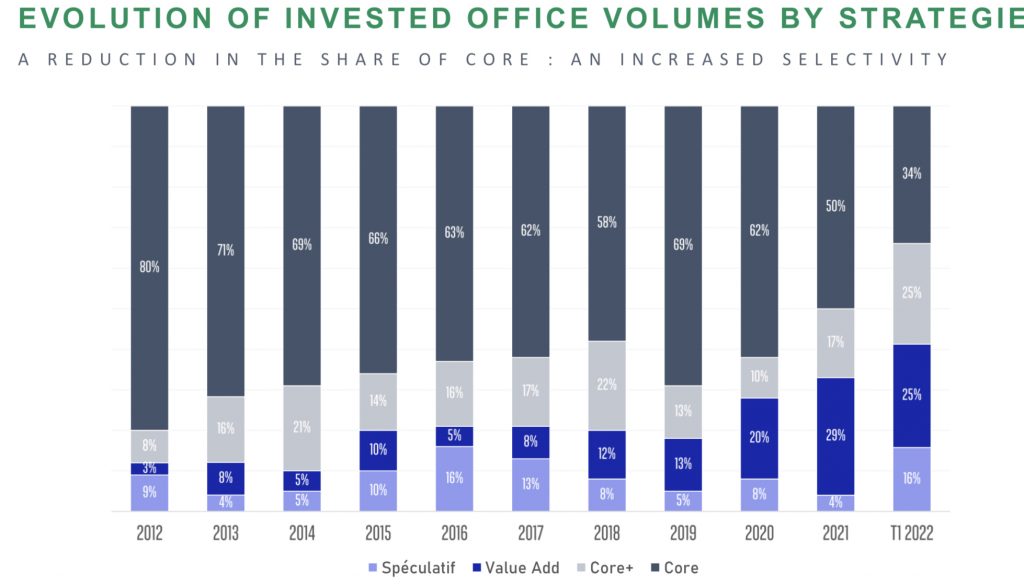

In Q1 this year there was a significant reduction in the share of core assets being traded, accelerating a trend that had become increasingly visible in the last few years.

The share of core investments in the office sector in Paris has declined from 69% in 2019, to 62% in 2020, to 50% in 2021, to a mere 34% in Q1 this year, according to BNP Paribas Real Estate figures. Value-add strategies, by contrast, have gone from 13% in 2019 to 25% in the first three months of 2022.

Same upward trajectory for speculative investments, that have shot up from 5% of the total in 2019 to 16% in Q1 2022, while core+ strategies, which accounted for 10% in 2020 and 17% in 2021, this year are up to 25%.

“We’ve seen significant rental growth and low supply, so traditional core buyers are taking risks in Paris now,” said Rory Sheard, international director, Paris office investment, BNP Paribas Real Estate. “ESG factors are becoming key in investors’ decisions, and this is contributing to lack of product.”

As investors become more selective, the number of attractive properties is shrinking while the potential for stranded assets increases.

“There is a definite split between ‘bad’ assets and ESG-friendly assets,” said Raphael Tréguier, founder and managing partner, Kareg Investment Management. “Older buildings are not interesting and there are a lot of empty assets, even fully-let offices that are empty. We’re in a transition phase but there are still opportunities for agile players.”

Market polarisation is becoming a feature of the Paris office market.

“The good offices of tomorrow are better than those of yesterday, so some assets are inevitably left stranded,” said Sheard. “Distressed office properties are being re-invented as mixed-use assets, student housing or even last-mile logistics and people are seeing this as an opportunity.”

The problem is that, however willing and creative investors are prepared to be, they have to deal with the authorities’ slow-moving practices.

“Repositioning and change of use is on a 5-10 year timescale in Paris while the investment timeframe is a few months, so clearly there is an issue,” said Tréguier. “It is difficult to assess administrative risk because investors are not familiar with it.”

Another issue is increasing material and labour costs.

“There are question marks over redevelopment risks now, as construction costs are going up,” said Wallace. “As projects are delayed or cancelled outright, supply will inevitably be further curtailed. Lack of supply will translate into higher rents, which is why we see the medium-term opportunities rather than focus on the short-term risk.”