Counting the cost of market volatility

Research from MSCI reveals slowing real estate markets across Europe as a multitude of global headwinds begin to bite. Will Robson, Tom Leahy and Beatrice Ginieis report.

European property returns slowed again in the second quarter of 2022 from their record highs seen at the end of 2021 on the back of a largely industrial-driven post-pandemic recovery. Investment volumes also declined as the emergence of a multitude of risks caused some investors to pause and reassess the outlook for commercial real estate.

A decade of historically low interest rates had pushed huge volumes of capital into the property market as investors looked to profit from the real returns property could provide. However, high inflation, rising central bank interest rates, increased debt costs, falling consumer confidence, concerns over economic growth and war in Ukraine all point to a more febrile environment for investors to navigate.

Investment returns

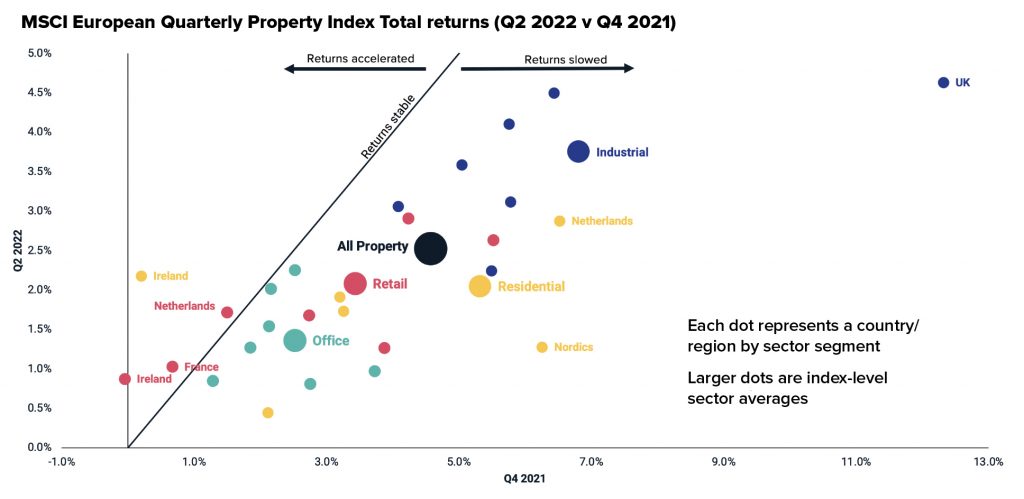

European real estate’s total returns decelerated to 2.6% in the second quarter of 2022, slowing further from 4.6% in the final quarter of 2021, according to the MSCI European Quarterly Property Index. The slowdown was broad based, led by the industrial sector, which came off particularly high returns at the end of 2021. UK industrial returns slowed the most, but this was still the strongest performance for any segment.

Residential in the Netherlands and Nordics also decelerated significantly from robust performance to the end of 2021. The only segments to see returns accelerate were Irish residential and retail in France, Ireland and the Netherlands. These segments improved from a low base in 2021 and experienced the lowest returns across the index in Q4 2021.

The office sector slowed the least in aggregate, but was also coming from a low base. Returns to the end of Q4 2021 were the lowest among the broad property types and have slowed slightly since then into Q2 2022.

Transaction activity – sectors

The apartment market was the only sector to escape the quarterly slowdown, with transaction volume up by a hair from a year earlier. In contrast, acquisitions of industrial property — the other darling of the post-pandemic market — fell 29% year-on-year, mirroring the slowdown in investment returns described above.

In an inflationary environment, the apartment sector is viewed as offering some protection against rising prices. Lease lengths are typically much shorter than in the commercial sectors, which provides an opportunity to reset rent levels more often than the three-to-five years typical elsewhere.

A surge in UK apartment sales, where the market had its best first half of the year, was driven by a slew of supersized deals for student housing, where volume topped €4 billion. More than €2.6 billion was also spent on residential for rent, which is also a record for the first six months of a year.

It was also a strong start to 2022 for UK office sales. Transaction volume rose 54% year-on-year in the first half, which contrasts strongly with France and Germany, Europe’s two other major office markets. French office volume was flat compared with 2021 and remains well down on pre-pandemic levels. German deal volume was down by 34% against the first half of 2021. Nevertheless, average prices for sold assets are slightly up on where they were last year in both Paris and the German ‘A’ cities, which suggests strong bidding for those buildings which have transacted.

After some signs of a post-pandemic recovery, the hotel market has stuttered again in the first half of 2022. Deal volume fell 28% versus the first half average in 2017-21, suppressed by concerns including the future of corporate travel and the impact of the higher cost of living on leisure travel.

Transaction Activity – Countries

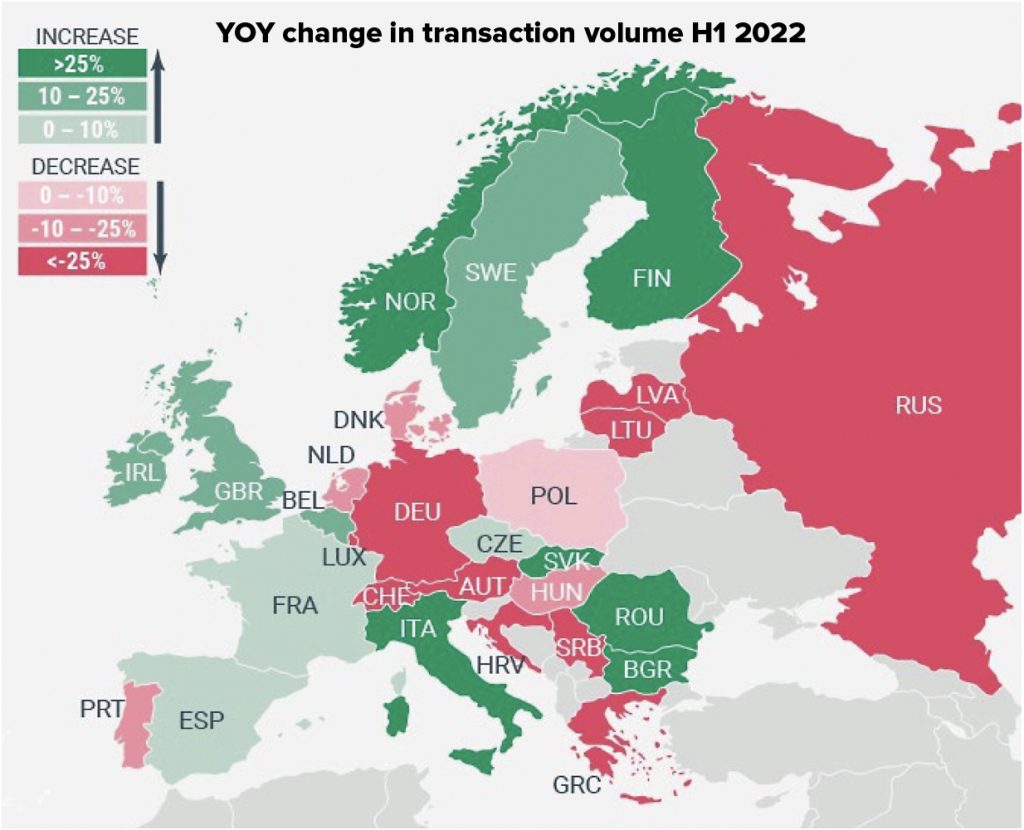

The German property market slowed very sharply in the first half of 2022 after a record 2021. Capital invested in German real estate fell 34% for the half-year and 56% for the quarter. Indeed, the second quarter was the slowest for investment across any quarter since 2012.

Buyers are clearly concerned about several risk factors that have emerged through the first half of the year: Germany’s reliance on Russian energy makes its economy vulnerable at a time of heightened geopolitical tensions between Russia and Nato, while rising interest rates have driven debt costs above prime transaction yields in some sectors. These headwinds have caused buyers and sellers to pause, resulting in a slowdown in dealmaking.

The UK presents something of a contrast with Germany. While the second quarter was down 11% year-on-year, first half volume was up versus last year and the 2017-21 average. There has been a strong rebound in office demand and transaction volume rose 50% YOY in H1 2022. Apartment deal volume rose 50% in the same period, and industrial deals were flat, but elevated compared with pre-pandemic levels.

Office deals have been buoyed by some supersized deals for central London stock. The standout transaction was the sale of the UBS office in March to South Korea’s NPS for £1.2 billion (€1.45 billion). However, it should be noted that 75% of 2022 central London office deal activity took place in the first quarter, with the second quarter being much slower.

French deal volume has also held up relatively well in the first half of the year and rose in comparison with the first six months of 2021. Office trades remain comparatively weak when looking to previous years and growth has been focused on the retail and the apartment sector. Indeed, it was a record start to a year for the nascent French apartment market and more than €3.6 billion was spent by mostly domestic players. CNP Assurances spent more than €2 billion acquiring an 85% share in Lamartine, a fund of more than 7,500 residential units.

Three top 10 markets recorded deal volumes that were up on both the quarter and half year. Italy, Ireland and Finland are all largely dependent on overseas capital to sustain liquidity in their transaction markets, so the loosening of pandemic travel restrictions has had a positive impact. Cross-border flows into Finland almost doubled, in Italy these flows rose 70% and in Ireland 36%.

Overseas buyers spent more than €3.6 billion on Irish property in H1 2022, a record start to a calendar year.

Capital flows

Cross-border acquisition volumes in aggregate were down 22% in comparison with the first quarter and down 16% YOY. This decline was largely due to a slowdown in acquisitions by non-European players, who spent €16 billion in Q2 2022, having averaged more than €24 billion in the previous three quarters. Again, the shifting investment landscape is having an impact on buyers, causing many to pause and reassess.

On the flip side, buyers from Singapore, Hong Kong and South Korea have been prominent in 2022. Singaporean players have been particularly active, spending close to €5 billion. The second quarter’s largest deal was the acquisition of the Singapore Press Holdings portfolio by Hotel Properties, Temasek and Mapletree for a price estimated to be in excess of €1 billion.

It is notable that spending from US- and Germany-headquartered players slowed sharply in the second quarter compared to the first. Quarterly flows from US-based investors slowed to the lowest level since the third quarter of 2020, in the teeth of disruption caused by the pandemic.

Spending by domestic players dropped to the lowest level since the third quarter of 2020. This is in part due to the slowdown in Germany, where domestic spending totalled just €5.1 billion in the second quarter, the lowest outturn since 2012.

French players also markedly reduced their acquisition activity in the second quarter of the year. But the reverse was true in Sweden, where local investors increased buying activity. Domestic spending in the UK also held up well. The largest deal of Q2 2022 was the sale of the Project Resolve portfolio, managed through the Janus Henderson UK Property Fund, to Oval Real Estate for £913m.

Signs of a slowdown

Headline property acquisition volumes held up well through the first half of the year. A rolling total for 2022 through to the end of June shows the market only just behind 2021 and well ahead of 2020, 2019 and 2018. However, encouraging as these headline numbers are, they don’t tell the full story, which is that the market appears to be slowing in response to a worsening economic outlook and rising interest rates.

Most obviously, second quarter transaction volume was down against the same period a year ago, when much of Europe was just emerging from lockdowns and the vaccine rollout was still in its infancy. Unusually, deal volume was also down on the first quarter — the market’s seasonality means second quarter volume is, on average, higher than the first quarter.

Digging deeper into the data suggests the market might be slowing faster than the volume numbers suggest. A preponderance towards large deals hides the fact that far fewer properties are trading across most major segments in the market. Indeed, an analysis of the main market segments in H1 2022 shows that the count of traded properties has fallen in 10 of the top 15.

Of the main exceptions to this weakness, growth in French retail and Finnish apartment sales has come from a very low base. Meanwhile, Swedish apartments recorded a very strong Q1 2022 before a marked deterioration in Q2, with the count of traded properties down by two-thirds.

It is important to note that deals are completing and more than €20 billion of commercial property transacted in June. Investment managers have raised billions in funds and the opportunity to capitalise on structural changes in how society interacts with the built environment remains.

But there seems to be an emerging preference for quality. This can be seen in the dichotomy between the drop in the number of offices to have traded in H1 2022 (compared with a five-year average) and the increase in transaction prices, as measured by the RCA Hedonic Series. This divergence shows that buyers are being much more selective, resulting in fewer overall trades, but that there is strong bidding for assets that do sell, resulting in upwards pressure on pricing.

Will Robson is global head of real assets solutions research; Tom Leahy is head of EMEA real assets research; Beatrice Ginieis is senior associate, real assets research, MSCI