Logistics’ 2022 volume to date ahead of 10-year annual average

GARBE’s latest Pyramid map shows how logistics is holding up with investors continuing to favour the sector, despite the recent global shocks. Paul Strohm reports.

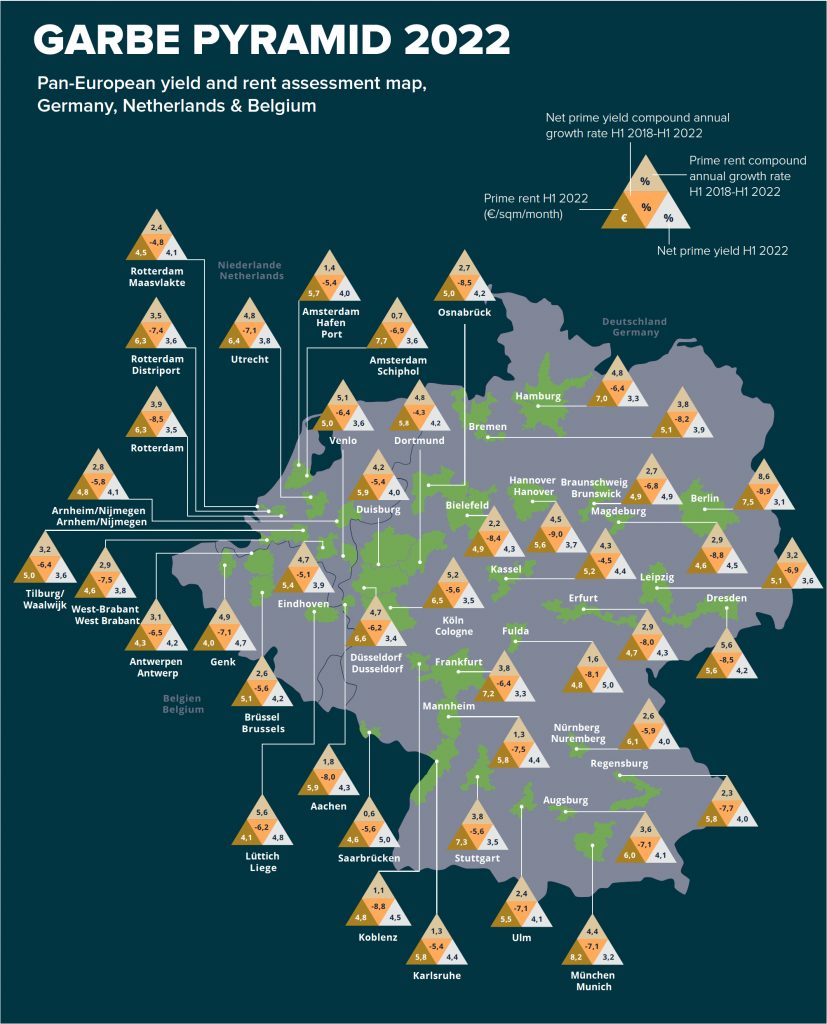

GARBE’s Pyramid Map 2022 shows 70% of markets covered had registered substantial growth since the end of 2021

Despite a series of challenges including the war in Ukraine, supply chain disruption before and after the pandemic, interest rate increases, and inflation, the logistics real estate sector remains robust.

The latest research from Hamburg-headquartered GARBE Industrial Real Estate has confirmed that both occupier and investment demand for the sector remain strong. “The market is still very eager to invest in logistics properties. We didn’t know if it would continue this year because we faced a war in Europe, ongoing supply chain distortions and other geopolitical factors,” notes Tobias Kassner, head of research at GARBE and member of the management board.

Related articles

- Global events highlight the need to rethink supply chains

- Logistics sector defies set-backs – rents and yields robust

“When we looked at the figures for the investment transaction market we saw the first quarter of this year was very good. It began to slow in April/May but, now we have all the data collected, we see that volumes for the first half of the year are close to the annual average for the last 10 years. Although it will not be a record-breaking year like 2021, it’s still a very good outlook,” Kassner says.

Rents are similarly robust it seems and Kassner points out that 70% of the markets covered by the GARBE Pyramid Map have registered substantial growth since the end of 2021, while rents were static for the remaining 30%. “The remarkable thing is, no region reported negative rental movement,” he adds.

The Pyramid Map looks at 122 different markets in 23 European countries, comparing rents and yields in each market and it examines the growth of these two metrics in the preceding half year.

Investors react to changing market environment

The trend was clear in Germany, where rents increased in 90% of the 29 German submarkets since the end of 2021. Around 10% of the market registered no changes during this period, but the fastest rental uplift was reported in Cologne (€0.6 per sq m), in Berlin, Duisburg, Dortmund, Munich (€0.5 per sq m in each case), as well as in Hamburg, Kassel and Düsseldorf (€0.4 per sq m each).

Although they remain enthusiastic about the sector, investors have not been unresponsive to the changing market environment. They are, for example, more cautious towards markets that lie geographically close to Ukraine’s borders. Furthermore, in response to the increasing cost of finance, investors are keener to invest in markets with lower yields, Kassner says.

“There’s still huge demand, for example, in the UK or Benelux or the western part of Germany – in the area that you could describe as the northern part of the ‘blue banana’,” he adds, referring to the theoretical Liverpool-Milan axis of urbanised areas in Europe.

“They also look, for example, more at Scandinavia, but also in the northern part of Italy where we saw a huge increase in transaction volumes, especially for the first half of 2022.”

The shifting economic context has been reflected to some extent in yields too.

“The core markets that the investors have focused on for the last few years were already very highly priced and here we can see a change because of the higher cost of financing,” Kassner says. “There’s a kind of decompression and we’re facing an upward shift of 10 to 20 basis points in some markets, and that applies to about 22% of the 122 submarkets we analyse for the Pyramid Map.”

Yield decompression

Decompression was noted in leading markets such as London (0.6%), Birmingham and London-Heathrow (both 0.3%), where prices were at a high level.

“While in those markets we are seeing a minor trend reversal, in 34% of markets we see no change,” adds Kassner. “However, in 44% of the 122 markets, yield compression is still evident because there is higher demand and because historically the yield level was substantially higher than in the top markets.”

This was the case in markets including Geneva (-1.0%), Piacenza (0.9%), Verona and Turin (-0.7%).

The picture is similar in Germany. Yields rose in 31% of the 29 German submarkets since the end of 2021, notably in the ‘Big Seven’ markets (Berlin, Cologne, Düsseldorf, Frankfurt, Hamburg, Munich and Stuttgart) as well as Duisburg and Erfurt (0.1%). Yields were static in 66% of the German markets and only in the Bielefeld logistics region – representing 3% of the German markets – did yields continue to decrease.

But Kassner adds that investors are very confident in logistics real estate as an investment product.

“When we assess the direction of the rest of the year we already see that confidence in the markets is quite strong, but there is a wait-and-see attitude where investors analyse on a day-to-day basis what we will face during the rest of the year.

“It is possible that there could be slight yield decompression in the top markets in the next year but for most of the markets where investment is focused at the moment there will be continued compression.”

One of the reasons for the continued popularity of logistics assets is that they compare favourably against other asset types. “When we see the yield level for logistics real estate and compare it, for example, with the risk-free level of bonds, we still see a huge spread so it’s still very interesting to invest,” notes Kassner.

Kassner adds that logistics also continues to compare favourably with office and retail real estate.

Examining market sentiment

For the current (fourth) edition of the Pyramid Map, GARBE expanded the scope of its research beyond numerical data to examine market sentiment and compare it against the figures. “We wanted to tap into the experience and market insights of, for example, the LinkedIn community as business professionals.

This was quite interesting because they didn’t know what our other research results would be.

“It was interesting to see, for example, 44% of respondents said yields remain constant, whereas when we summarised it, it was somewhat less than 34%. On the other hand, 31% of the panel said yields will start to decompress whereas the actual figure was 22% of markets. But this was still quite a good correlation so I think we will use questionnaires in the future as another element of research.”

Kassner notes that the different conclusions of the investment and occupier communities were also revealing. “We haven’t yet seen uncertainties among our tenants for example, with the exception of e-commerce in Germany.”

‘For most markets where investment is focused at the moment there will be continued yield compression.’

Tobias Kassner, GARBE

E-commerce companies built large space surpluses during the pandemic to be ready for when consumers started spending again, as well as resuming holidays. However, rising inflation, the energy crisis and the war in Ukraine have led to increased uncertainty and a fall in consumer confidence. “We now have one of the lowest levels of consumer confidence since records began and e-commerce is not going quite so well.”

But this is likely to be just temporary, he says, as e-commerce penetration in Germany has some way to go even if it is on pause for this year.

Although e-commerce occupier demand as gone off the boil, GARBE and some of its competitors have zero vacancy, partly due to the high levels of confidence among the “bread and butter” occupiers – logistics operations.

Reshoring and nearshoring

Another source of increased demand is the growing propensity for nearshoring, reshoring and inshoring as companies respond to the increased level of threat to their supply chains.

“There has been increased discussion about reshoring and nearshoring trends for a few years, and before the pandemic,” says Kassner. “The geopolitical tensions between the US and China, increased labour costs in China, the closure of the Suez Canal, then the Ukraine war, zero covid policy in China, concerns about Taiwanese chip production, have left so many companies thinking about restructuring their supply chain.

“We see huge potential for the eastern European countries, southern European countries and others nearby such as Turkey and North Africa where there’s workforce available and low labour costs.”

A glut of empty space seems to be unlikely, says Kassner and from the supply side, the difficulty in obtaining new stock and sites for develop continues to be a constraint on over development.