SHHA Summit: Spain’s demographic ‘tsunami’ to drive nursing home demand

Spain is the canary in the coalmine when it comes to senior housing and healthcare, delegates heard at the fourth SHHA Summit, organised by the SHHA and Real Asset Media, which took place recently in Brussels.

“Spain’s baby boom happened earlier than in other EU countries, with large cohorts born in the 1940s, so what we are seeing now in Spain will also happen in the rest of Europe”, said Andreu Huguet Llull, co-CEO, Healthcare Activos, a specialised REIT. “We are witnessing a demographic tsunami.”

Spain is one of Europe’s fastest-ageing nations: currently 21.1% of the population is over 65, but that percentage will rise to 36.1% by 2050. People over 80 years of age are now 6.5% of the population, but they will be 13.9% by 2050.

“Nursing homes have been full since 2024, and this demographic wave will drive nursing home demand for decades to come”, said Huguet Llull. “By 2050 the old age dependency ratio in Southern Europe is projected to reach 61%, the highest in the EU.”

The traditional population pyramid has been inverted and there are now more than 100 people over 65 for every 100 children under the age of 15. As life expectancy reached 83.4 years in 2025 and is forecast to rise further, a significant increase in demand for residential care is expected in the coming years.

“In order to create the 204,000 new beds needed an investment of €20 billion in the next ten years is required”, said Huguet Llull. “The undersupply is very clear, but it is impossible to develop this kind of capacity in Spain for many reasons.”

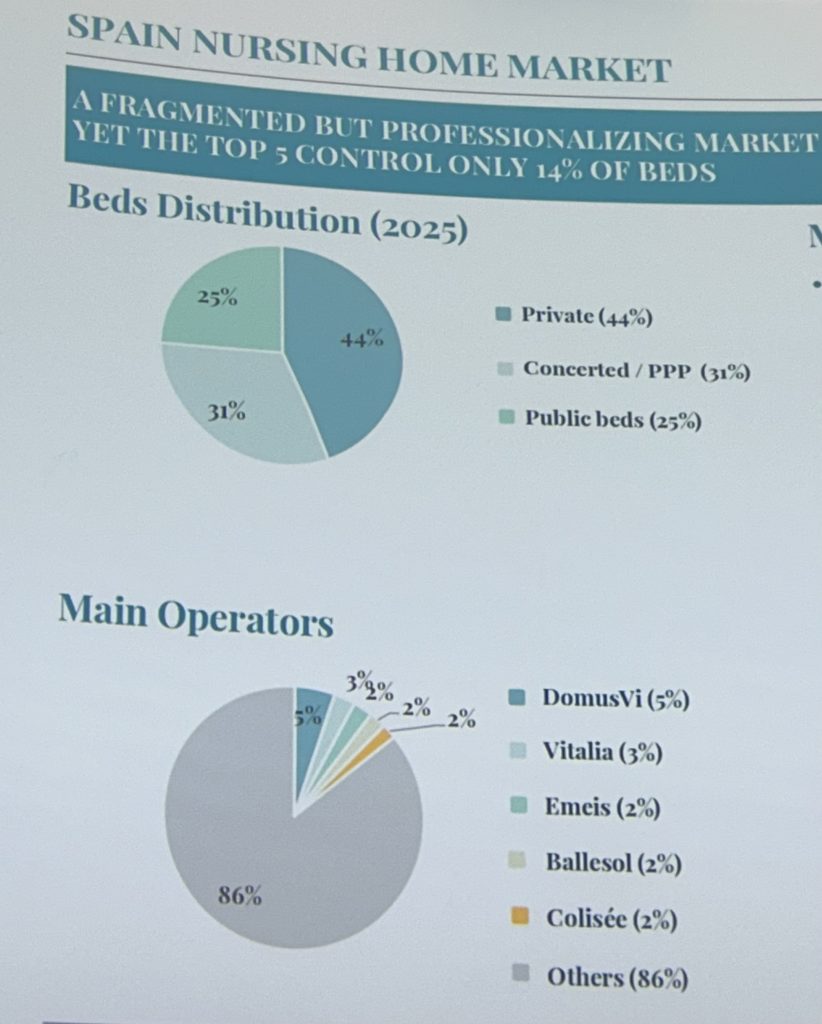

The market is dominated by private operators but it is also very fragmented, as the top five control only 14% of beds. Many small, single site operators coexist with large national and international groups. DomusVi, the biggest, has a 5% share of the market and Vitalia is second with a 3% share.

“Profitability has improved in the last couple of years, and progressive tariff increases have restored and expanded operator margins,” said Huguet Llull. “Leading operators’ EBITDAR margins are 30% plus, but Spain is not the Eldorado.”

Rising personnel costs, driven by wage inflation and increasing staffing ratios due to regulatory requirements, are the key structural risk. Despite having the most competitive construction industry in Europe, costs have increased by 30% in the last two years.

Another issue is Spain’s fragmented territorial landscape, with a specific regulatory framework and labour agreement in each region. Equally stark variations are seen in the average daily rates for nursing homes, with prices that vary from €95 in Northern regions to €60 in Castilla La Mancha.

Anyone interested in a Spanish greenfield strategy needs to price in the following risks: construction cost inflation, land scarcity and high prices, operator costs going up and the need to future-proof the asset by getting the right ESG certifications.

“Structural barriers rather than lack of capital are the main barriers to building new capacity in the sector”, said Huguet Llull. “As there are 19 different labour and building regulations, it is essential to understand local dynamics and have good people on the ground.”