PwC: Data centres are”permanent critical infrastructure”, not just a short-term boom

Data centres have moved decisively beyond their origins as a niche real estate play and are now being reshaped as critical infrastructure assets, deeply intertwined with energy systems, geopolitics and national economic strategy.

“Five or six years ago, data centres were still discussed as a niche,” Thomas Veith, partner and global real estate leader at PwC, told a packed room at a Real Asset Media briefing hosted by PwC in London on 20 January. “Today, they are consistently the number one sector to watch from a real estate and real assets perspective — across all regions,”

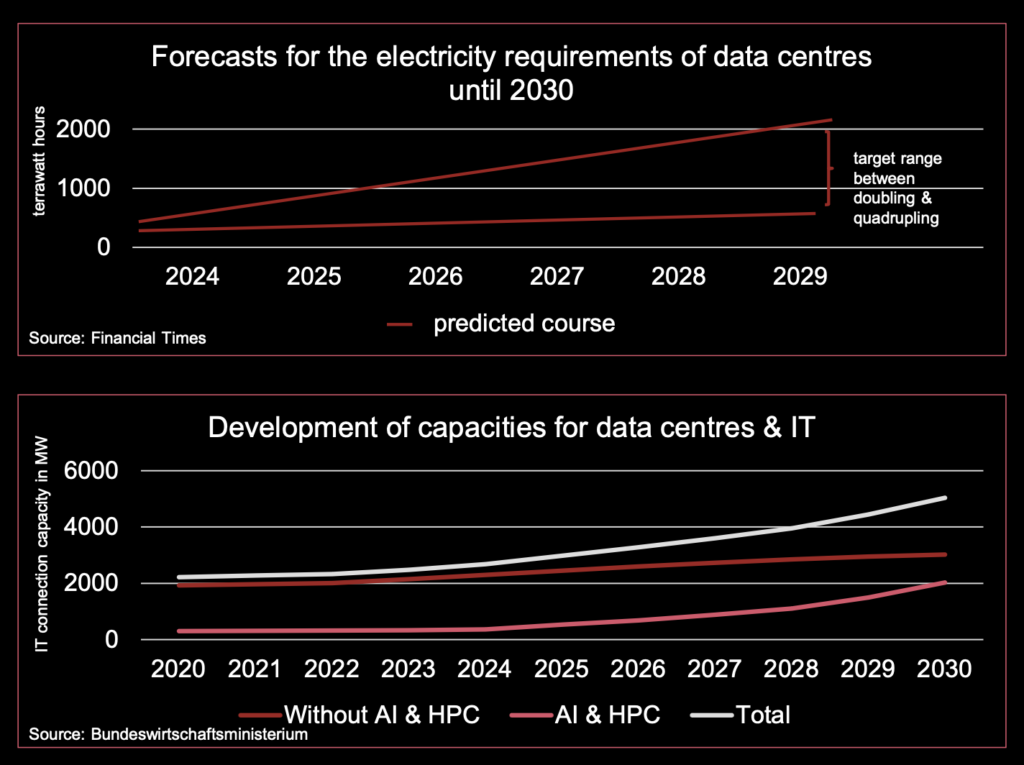

Global capacity is expected to double from roughly 100 gigawatts today to around 200 gigawatts by the end of the decade, even allowing for conservative assumptions. For investors, this implies not only sustained capital deployment but also a need to rethink underwriting models, lifecycle assumptions and risk allocation.

One of the most striking changes Veith highlighted is the rapid escalation in project scale. Where early institutional interest focused on relatively modest facilities, the market is now dominated by hyperscale and AI-driven developments requiring capital commitments of hundreds of millions — and in some cases billions — of euros.

“A lot of investors are now asking why these tickets have become so large that they are sometimes too big even for them,” Veith noted. “At the same time, the complexity has increased enormously, not just from a construction perspective, but in terms of technology, risk and long-term value.”

This shift is forcing the real estate industry itself to upskill. According to Veith, investors and developers are still on a learning curve when it comes to understanding the full implications of data centres — from power resilience and cooling to security, planning risk and lifecycle management.

While artificial intelligence has become the most visible catalyst for data centre demand, Veith cautioned against viewing the sector purely through the lens of AI hype. Training large language models is energy-intensive and has amplified demand, but the structural drivers extend much further.

“AI is an important driver, but it is only one among many,” he said. “There is still a fundamental transformation underway as industries, healthcare, mobility and governments all become data-driven.”

PwC’s latest global CEO survey underscores this point. Only 12% of CEOs believe they are currently capturing meaningful value from AI, suggesting that the majority of organisations are still at an early stage of adoption, with significant implications for future compute demand.

“Even if you assume some of today’s projections are inflated by hype, there is still a clear, fundamental growth perspective from the user and tenant side,” Veith said. “That means continued demand for data centre capacity.”

From real estate to sovereignty infrastructure

Perhaps the most profound shift, however, is political. Veith described how data centres are increasingly viewed as instruments of sovereignty, economic positioning and control — not simply income-producing assets.

“Digital infrastructure has become power infrastructure,” he said. “Control over data, cloud and AI creates strategic dependencies between states, regions and corporations.”

This dynamic is playing out differently across regions. In the US, data centres are closely linked to market-driven scale and technology leadership. In China, they function as tools of state control and internal stability. In the Gulf, they are part of diversification strategies away from hydrocarbons, leveraging abundant energy and capital. Europe, meanwhile, faces a more constrained path, balancing strong regulation and data protection with the need to remain competitive.

“Globally, data centres are tools of power projection and economic positioning, not just real estate developments,” Veith said.

As the asset class matures, energy access has become the defining constraint. Power availability, timing and resilience — rather than land cost alone — now dictate site selection. Grid access is emerging as the real bottleneck, pushing development away from traditional hubs such as London and Frankfurt towards secondary locations with greater headroom.

“Power is not just about volume,” Veith said. “It’s about availability, timing and resilience, and increasingly about social acceptance.”

Local opposition is also growing. Data centres create relatively few jobs while consuming large amounts of energy and water, raising questions for municipalities about what they gain in return. As Veith put it, “acceptance is increasingly what decides approvals.”

Despite concerns around valuation cycles and AI-driven exuberance, Veith rejected the idea that data centres represent a short-term boom.

“Data centres are no longer a cyclical real estate story,” he said. “They are becoming permanent critical infrastructure with long-term political relevance.”