Chelsea F.C. and DAMAC launch the world’s first football-branded residences in Dubai

Chelsea Football Club has partnered with Dubai-based luxury developer DAMAC Properties to launch Chelsea Residences by DAMAC, the world’s first football-themed branded residential project.

The waterfront scheme in Dubai Maritime City will comprise over 1,400 homes in six towers. Construction will start in 2025 and be completed by 2029. Unit prices begin at 2,170,000 UAE Dirham ($591,000).

Announced at a launch event at Stamford Bridge in London, the project blends Chelsea’s sporting legacy with high-end residential living. It offers amenities such as a rooftop football pitch, Chelsea Sports Bar, Athlete Performance Centre, cryotherapy suites, an aerial yoga studio, a private cinema, Chelsea Blue Beach Club, and forest relaxation pods.

“This partnership with DAMAC signals an exciting chapter in the Chelsea story, bringing our club’s spirit and prestige into the real estate world,” said Todd Kline, president of commercial at Chelsea F.C. “Chelsea Residences by DAMAC will give our fans and discerning buyers the chance to become part of the Chelsea legacy in an entirely new and extraordinary way.”

The homes will offer 270-degree views of the Arabian Gulf and the Dubai skyline. One-, two- and three-bedroom layouts are available, and lifestyle offerings will include a mono-diet café and a series of ‘Captain’s Table’ events hosted by Chelsea legends.

“Our collaboration with Chelsea F.C. is a first-of-the-kind and offers an unmatched residential opportunity for buyers who value exclusivity and quality,” said Amira Sajwani, managing director of sales and development at DAMAC.

The project launch attracted interest from UK-based investors and Chelsea supporters, reflecting wider international demand for branded residences.

Dubai remains one of the most attractive markets for international buyers, offering average gross rental yields of 7% alongside zero property tax, no capital gains tax, and no income tax on rental income. The British expatriate population in the UAE now exceeds 180,000.

Founded in 2002, DAMAC has delivered over 48,000 homes globally and is known for previous partnerships with Versace, Cavalli, Fendi Casa, and de GRISOGONO. The Chelsea project marks its latest move into lifestyle-led real estate development at the intersection of brand, sport, and luxury living.

Analysis: The market for branded residences has evolved from a niche experiment into a fast-growing global asset class attracting high-net-worth individuals, developers, and, increasingly, institutional investors.

Once limited to resort destinations and trophy projects, the sector has diversified. Lifestyle-branded residences — distinct from hotel-branded developments — are now proliferating in global cities, emerging markets and second-tier hubs. These schemes are anchored not in hospitality operations but in partnerships with fashion houses, automotive marques, and design brands, reshaping luxury living and real estate investment strategies.

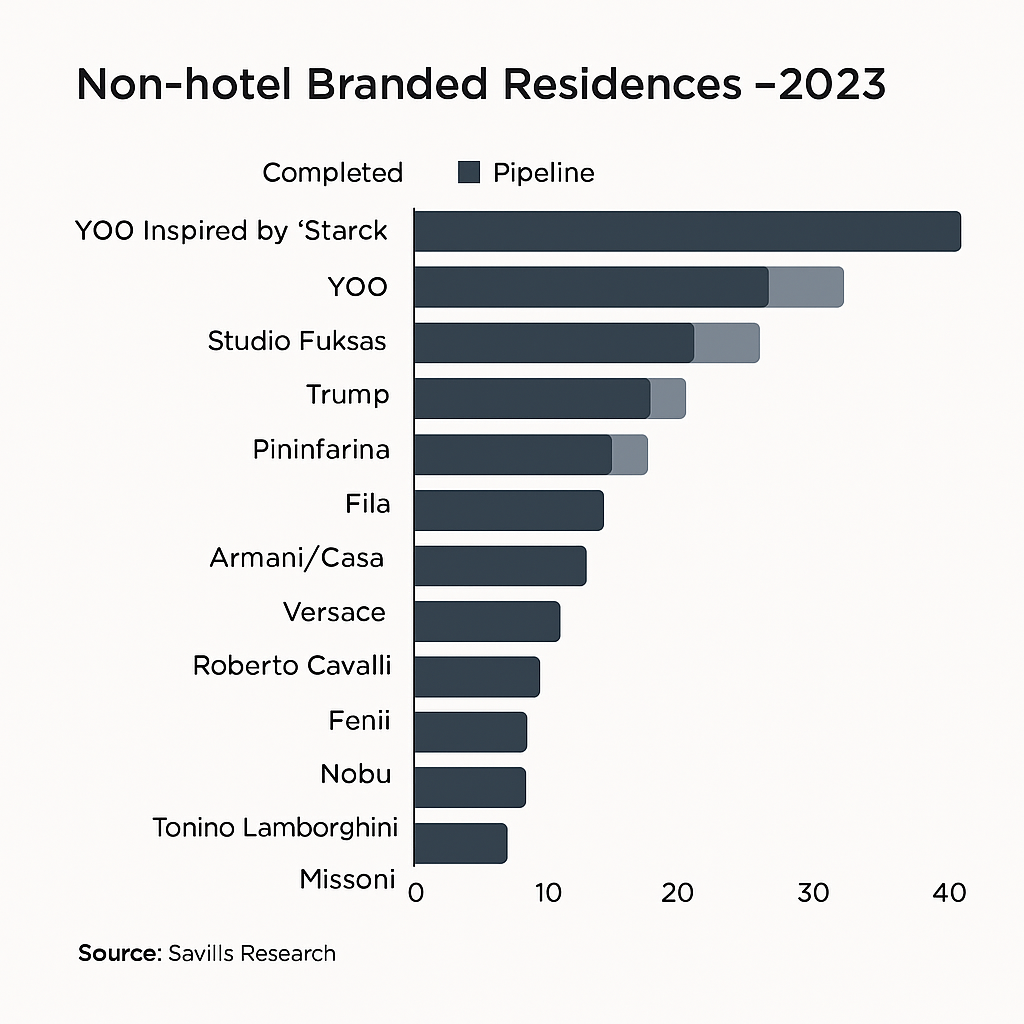

According to Savills, the number of branded residential schemes globally has surged from 311 in 2010 to over 690 in 2023, with the total forecast to exceed 1,400 by 2031. Lifestyle-branded schemes now represent 19% of the market, up from 11% a decade ago. That share is expected to grow as non-hotel brands expand their footprint.

While the United States remains the most significant national market, Dubai is now the leading city globally, followed by Miami, New York and London. Lifestyle-branded projects in Dubai and Miami are especially prominent, with developers leveraging brand identity to target international buyers.

London has seen launches such as the Armani Residences at Admiralty Arch and DAMAC’s Versace-branded scheme in Nine Elms. New York, Los Angeles (with Mercedes-Benz and Baccarat), Bangkok (Tonino Lamborghini) and Manila (Armani/Casa, Missoni) are also active.

Saudi Arabia is emerging as a serious contender, driven by its Vision 2030 economic diversification agenda. Riyadh has seen new launches, including Etoile by Elie Saab and Armani-branded villas in Diriyah. Versace Home is also involved in a luxury project in the capital, reflecting the Kingdom’s ambition to become a regional hub for ultra-premium living.

These schemes are typically structured as joint ventures between developers and brand licensors, combining co-branded marketing with elevated design, strong resale positioning, and curated lifestyle amenities. Unlike traditional hotel-branded residences, which are often linked to on-site hospitality services and resort management, lifestyle-branded properties focus on exclusivity, design, and cultural alignment.

Lifestyle-branded residences have also proven attractive to institutional investors. Sovereign wealth funds, Gulf family offices, and private equity vehicles are backing projects in Dubai, Miami, and London. Dedicated funds targeting luxury and lifestyle-branded residences have been launched, including the $3bn Driftwood Lifestyle & Luxury Fund. Driftwood Capital also closed a $1.2bn portfolio consolidation of branded hospitality assets in early 2024.

Cain International is developing One Beverly Hills, a $5bn mixed-use scheme with branded residences. The scheme is backed by a $2bn funding package and a $300m mezzanine loan from VICI Properties.

Returns are a key draw. Globally, lifestyle-branded residences offer price premiums of around 30% on initial sale values, with strong resale values and secure income streams. This compares favourably with hotel-branded residences, where price premiums tend to be lower, typically around 20–30% over non-branded equivalents.

According to Knight Frank, lifestyle-branded schemes can command premiums of 25–35% — and in Dubai, uplifts can reach as high as 102% in prime cases. These schemes often generate stronger resale performance and higher yields due partly to their design-led appeal, cultural resonance and reduced reliance on hospitality operations.

Rental yields for lifestyle-branded residences typically range from 3–4% in established urban markets like Paris or New York to 6–8% in emerging hubs like Dubai or Manila, depending on location, brand equity, and amenity offering. The branded element provides investors prestige and risk mitigation through quality assurance and service continuity.

Recent growth markets include India, where the luxury residential segment is projected to grow from $44.11 billion in 2025 to $118.30 billion by 2030 at a CAGR of 21.81%, driven by the expansion of the ultra-high-net-worth population.

In Southeast Asia, Vietnam has seen a 210% rise in branded residence developments, while the Philippines continues attracting investment from domestic and overseas buyers.

In Europe, activity remains focused on London, Paris and southern lifestyle markets such as the Algarve and Costa del Sol. Urban centres in Spain, Italy and Germany are gaining interest as developers seek to stand out amid rising supply. Second-tier cities with brand resonance are also coming into play.

Momentum is building in new markets across multiple cities. Cape Town, Athens, Rio de Janeiro, São Paulo, Mumbai and Ho Chi Minh City are among the next cities likely to host lifestyle-branded schemes driven by rising regional wealth, tourism growth, and limited legacy competition. As land becomes scarcer in mature hubs, developers are looking further afield for brand-aligned opportunities. Fashion, automotive and jewellery brands have led the trend, but tech, retail and media names may follow.

For developers and investors alike, lifestyle branding has moved from novelty to strategy — unlocking value through emotional resonance, global familiarity and experiential living. With their design-led ecosystems and loyal customer bases, tech firms such as Apple are often cited as potential entrants into this space — a move that would further blur the line between brand and lifestyle.