Resi will retain its attraction despite yield increase in 2023

Yield compression can be expected in the residential sector from next year, according to research from investment manager AEW.

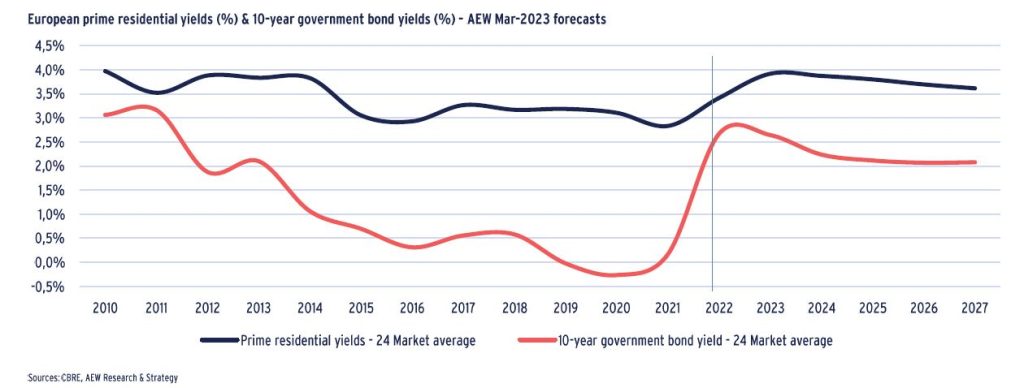

The firm forecasts that residential yields will increase 50 bps this year but this will be followed by yield compression from 2024.

The sector will retain its appeal to investors, and its defensive characteristics along with its ability to hedge inflation through income growth, remain the principal attractions. Meanwhile, the long-standing undersupply of residential property throughout Europe will become even more acute, squeezed on one hand as higher interest rates increase demand for rented housing, and on the other by environmental legislation which will reduce the amount of lettable stock.

“A combination of rising mortgage rates supporting the rental market, a post-Covid return to cities underpinning the secular urbanisation trend, as well as positive household formation growth will continue to put further strain on already constrained supply,” said AEW director of research and strategy Irène Fossé.

“We expect this long-standing shortage of rental housing to become even more acute in the short term as EPC rating and sustainability regulations become effective and priced in by both occupiers and investors. These are already driving green premia for those assets with the best credentials.”

Meanwhile, rising construction and finance costs will weaken developers’ profit margins, further reducing supply.

Strong rent growth can be expected across Europe as a result of these trends and AEW forecasts that for the 2023-27 period, prime residential rental growth will be about 3% per year, in line with logistics but higher than office and retail.

AEW also predicts that recently introduced rent caps designed to protect tenants against inflation-linked rent indexation will be temporary and will not inhibit long-term rent growth.

Opportunities may arise as some investors experience difficulty with debt refinancing, AEW predicts. Furthermore, as residential REITs have traded at a significant discount to their NAVs due to above average leverage, some of them may be forced to sell assets to rebalance portfolios.

“The sector’s defensiveness can play a positive role in diversified portfolios, in part based on its inflation hedging characteristics,” said AEW’s head of research and strategy Hans Vrensen. “Attractively re-priced buying opportunities should emerge over the course of this year and into 2024,” he added. As well as residential REITs needing to rebalance their capital stacks, higher interest rates making it difficult for some investors to refinance, this will be attributable to undercapitalised landlords that are unable to invest in greening their portfolios.