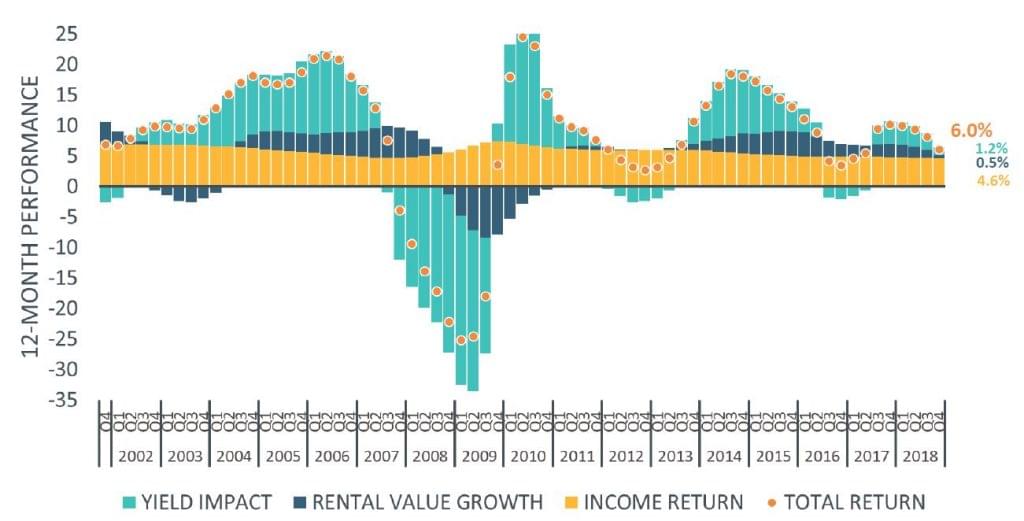

MSCI: Q4 UK capital depreciation marks inflection point

Capital growth in UK commercial real estate turned negative in the final quarter of last year, after successive moderated growth since Q4 2017, to limit annual investment returns for 2018 to 6.0%, according to MSCI data.

Aside from the EU referendum ‘blip’ of Q3 2016 – which saw a raft of retail property fund fire sales depressing capital growth for the quarter before rebounding – Q4’s capital depreciation was the first fundamentals-driven decline recorded since 2012. MSCI’s data shows that the quarterly depreciation was comprised of a -0.2% fall in rental value growth and a -0.1% fall in yield impact, a proxy for investor sentiment.

Overall, the 0.8% total return in Q4 was the lowest for six years, excluding the Q3 2016 ‘blip’, and was driven by significant deterioration in the retail sector. Q4 retail total returns slipped -1.6%, taking annual returns to -0.5%. By comparison, offices returned 1.5% in Q4 and 6.2% for the full 2018, while industrial and retail – again, the sector star for the year – recorded 3.3% and 16.4%, respectively.

Multi-asset class context

Relative to other asset classes, UK commercial real estate performed well. Real estate funds, as measured by the MSCI/IPD UK Quarterly Funds Index, was the top performer with 6.5%, followed by 1.6% for fixed income, as captured by JP Morgan. Listed real estate stocks posted heavy double-digit losses of -15.8%, while equities slipped -8.8%, both measured by MSCI indices.

On a three-year basis, direct real estate is narrowly second, at 6.5%, behind equities, at 6.7%. Real estate fund performance was 6.4%, followed by 3.7% by bonds. Property stocks slipped -5.3%. Over five and 10 years, direct real estate outperformed other assets classes with 10.1% and 9.0%, respectively.

The cycle long view

Taking a longer-term perspective, total returns in UK all-property commercial real estate hit a cycle high watermark of 18.1% in 2014. Over the subsequent 18 months to Q2 2016, 12-month rolling total returns have weakened successively each quarter. The EU referendum vote then triggered a retail investor-led panic which drove fire-sales to meet redemption requests, forcing quarterly returns down to levels not seen since 2012.

While investment performance rebounded at the turn of 2017, this was only to levels close to pre-EU referendum performance. Thereafter, the 12-month rolling total returns have continued to slip to the lowest levels since 2012, excluding – of course – the Brexit ‘blip’.