MSCI: Data centres outperformed all asset types but future remains uncertain

Data centres have outperformed all other private and public asset types since 2011, according to new MSCI research, transforming the sector into a mainstream investment for large institutional investors, but “long-term outcomes remain uncertain”.

Data centres have generated annualized returns of 23.1% since 2011, MSCI research shows. Their long-term performance compares with an 18.1% return from global private equity funds, a 12.1% return for private infrastructure assets and a 10.1% return from public equities.

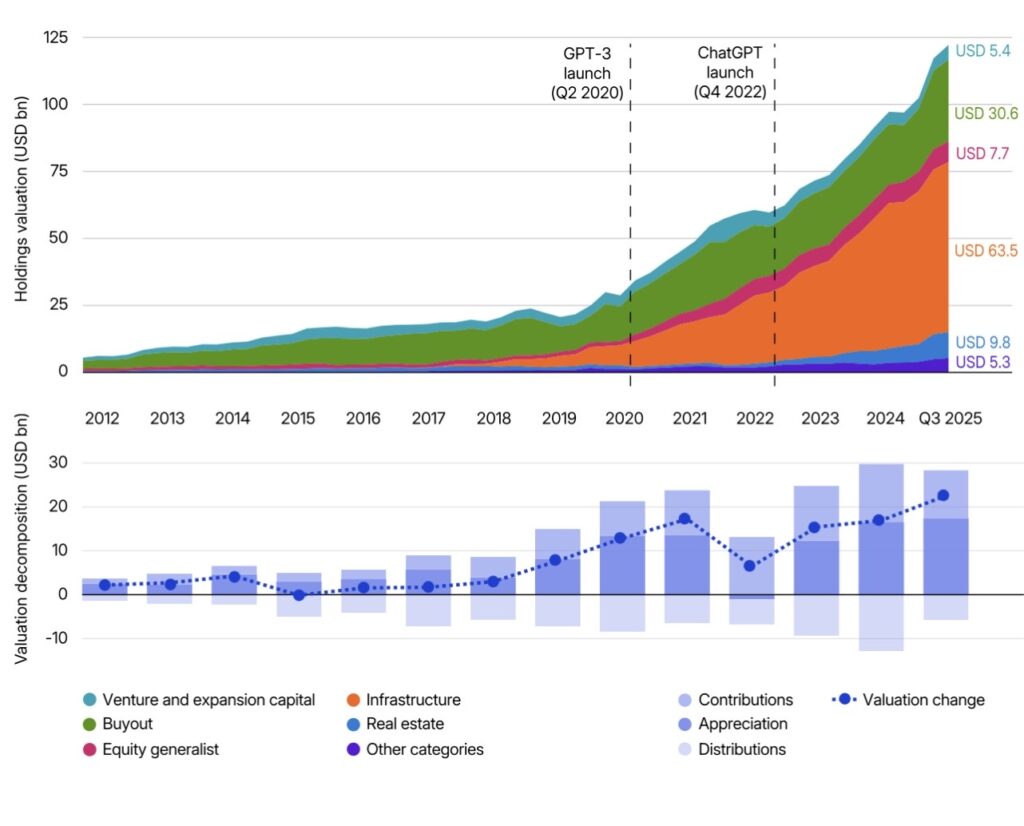

Data centres have become a key institutional allocation in private markets, with exposure across infrastructure, real-estate and private-equity closed-end funds totalling $122 billion as of Q3 2025.

Globally, construction starts of data centres have risen from $60 billion in estimated completed value in early 2020 to about $340 billion by 2025, according to MSCI Real Capital Analytics data, reflecting the sector’s rapid scaling in recent years.

The researchers analyzed 584 data-centre companies and assets held by closed-end private-capital funds in the MSCI Private Capital Universe dataset, assessing capital investment, valuation growth and realized performance. The study covered companies that build, operate and enable digital compute across five categories: hyperscalers, colocation and wholesale operators, cloud providers, network-infrastructure companies and supporting software and service firms, with an aggregate valuation of $122 billion.

The data-centre investment universe has evolved into a multi-asset-class segment, with exposure expressed across a range of strategies. Real estate and infrastructure represent 60% of total exposure ($73.3 billion). Equity strategies account for a further 36% of the investment universe, reflecting buyout, expansion capital and venture capital. While real-asset strategies provide direct exposure to physical infrastructure, equity strategies capture a broader set of companies across the data-centre value chain.

Following the release of ChatGPT in Q4 2022, investment momentum spread. Infrastructure valuations continued to rise, while real-estate exposure expanded alongside it, reflecting parallel growth to support increasing AI-driven compute density, power demand and energy intensity.

The pace of valuation growth was particularly pronounced in 2023 and 2024. Aggregate valuations increased by approximately $33 billion during these two years. At the same time, the sector generated $22 billion in distributions — that is, realized outcomes for investors.

Data-centre performance has been realized through large-scale institutional investments rather than niche allocations. Data centres have evolved into a mature and institutionally anchored segment, supported by sustained capital inflows, asset appreciation and meaningful distributions. Participation by large managers is evidence of the segment’s move from a niche play to a mainstream institutional allocation.

Long-term outcomes remain uncertain, however, MSCI says. Future performance may hinge on sustained technological adoption, alignment between the expansion of data-centre capacity, and demand and the ability to manage emerging operational and scaling constraints.

MSCI states therefore that “investors should remain aware that while data-centre exposure spans multiple asset classes, allocations are anchored to the same driver — computational demand — meaning that apparent diversification may not fully mitigate thematic concentration risk”.